Audit committees are responsible for evaluating the effectiveness of policies and procedures designed to ensure management’s representation of your company’s financial condition is true and accurate. Auditing is a critical step in any type of ethical, social audit, performance audit, or ESG assessment that demands an objective conclusion.

Policies include oversight responsibility for the integrity of financial reports, management control systems, and risk assessment processes. This group of individuals is also responsible for overseeing the auditing function, which includes consideration of the integrity of internal controls over financial reporting. The audit committee will not typically be involved in day-to-day operations or in making operating decisions that could have a material impact on us. For this reason, it is important that audit committee members have an understanding of external auditing standards as well as an appreciation for how risks affect our business practices.

- What can you expect from your audit committee?

- What is the role of the audit committee?

- Who should be on an audit committee?

- How should an audit committee work?

- What are some challenges that an audit committee might face?

- Who is involved in the process of conducting an audit?

- What is the role of the audit committee?

- What is the outlook for audit committees?

- What is a sustainability audit committee?

- What is the role of the chief financial officer (CFO) on an audit committee?

- What is a risk assessment process?

- What are some examples of major risks?

- Why does a company need an audit committee?

- What is the role of the committee?

- 4 typical audit committee members

- Why do companies need independent auditors?

- Who is required to have an audit committee?

- What happens in an audit committee meeting?

- How does the audit committee help in financial reporting?

- What are the disadvantages of an audit committee?

- What are audit committee roles?

- In conclusion the internal audit function

- Caveats, disclaimers & audit committees

What can you expect from your audit committee?

You should expect to see the audit committee discuss and oversee each major risk that your company faces, such as those related to financial reporting. Such risks include fraud, legal, regulatory (both internal and external), operational (reliability of information systems or business disruption), and reputational (e.g., brand and reputation protection).

What is the role of the audit committee?

The role of the audit committee is to supervise the auditing function, which includes oversight responsibility for the integrity of financial reports, management control systems, and risk assessment processes. This group of individuals is responsible for evaluating the effectiveness of policies and procedures designed to ensure that management’s representation of your company’s financial condition.

Who should be on an audit committee?

An audit committee should have at least three members who meet the requirements of being an “audit committee financial expert.” The FAST Act also requires that audit committees include independent directors.

An audit committee is made up of board members with expertise in finance, accounting, and risk management.

How should an audit committee work?

An audit committee should have an annual schedule of meetings, written meeting agendas, formal meeting minutes, and other relevant materials. It is very important that the committee discusses and oversees each major risk we face as a company, such as those related to our financial reporting.

What are some challenges that an audit committee might face?

There could be a challenge in determining whether management has effective internal controls over financial reporting since this responsibility is not typically included in the scope of a board’s activities. Other challenges might include reconciling unfamiliarity with your business and industry or pressures from management to avoid conflict.

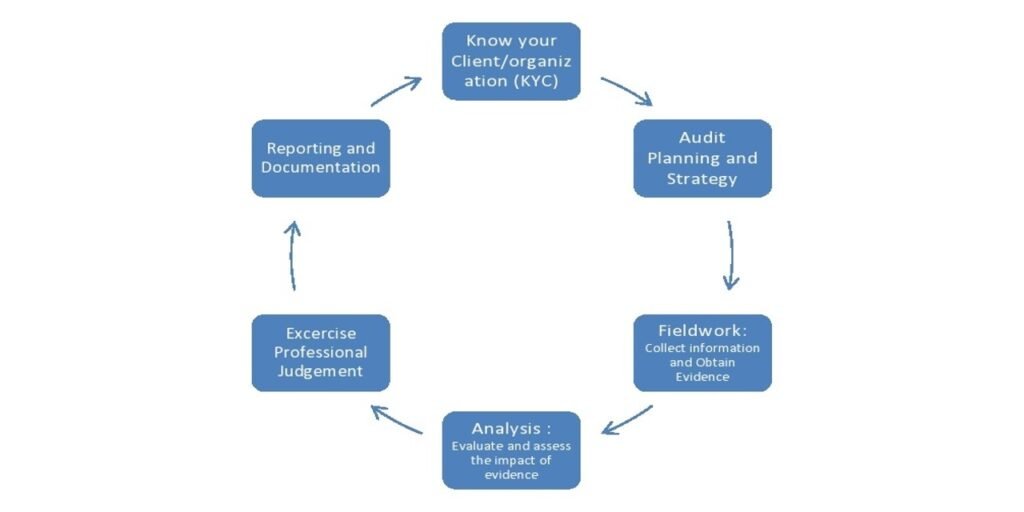

Who is involved in the process of conducting an audit?

An audit committee is made up of board members with expertise in finance, accounting, and risk management. With external auditors, committees typically have a designated audit committee chair and a liaison from the board’s nominating and governance committee.

What is the role of the audit committee?

The role of the audit committee is to supervise the auditing function, which includes oversight responsibility for the integrity of financial reports, management control systems, and risk assessment processes. This group of individuals is responsible for evaluating the effectiveness of policies and procedures designed to ensure that management’s representation of your company’s financial condition is true and accurate.

What can you expect from your audit committee?

You should expect to see the audit committee discuss and oversee each major risk that your company faces, such as those related to financial reporting. Such risks include fraud, legal, regulatory (both internal and external), operational (reliability of information systems or business disruption), and reputational (e.g., brand and reputation protection).

What is the outlook for audit committees?

With increased legislative and regulatory focus on audit committees, their roles and responsibilities will only increase. This means that companies will need to think about how they structure such committees so they receive adequate oversight of financial reporting risks.

What is a sustainability audit committee?

Sustainability Audit Committees are made up of key stakeholders including business, finance, human resources, IT, marketing and supply chain. The purpose is to help create an environment that promotes success in all areas of the company – socially, environmentally and financially.

What is the role of the chief financial officer (CFO) on an audit committee?

The CFO is a key member of the audit committee as they have an understanding of financial reporting and can assist with tasks such as reviewing management’s representations with respect to the company’s internal controls over financial reporting. The CFO will also provide insight into areas that could be improved upon.

What is a risk assessment process?

A risk assessment process is a framework on how to identify, assess, and manage risk. Risk management covers the entire organization, not just financial risks.

What are some examples of major risks?

Some examples of major risks include legal (e.g., class actions or contract disputes), regulatory (e.g., new government requirements), operational (e.g., IT outages), reputational (e.g., brand and reputation protection), and fraud.

Why does a company need an audit committee?

Companies need a quality audit committee for several reasons. For one, the audit committee is responsible for supervising the auditing function which includes oversight responsibility for the integrity of financial reports. Secondly, they are responsible for evaluating the effectiveness of policies and procedures designed to ensure that management’s representation of your company’s financial condition is true and accurate. Without an audit committee, there is no one to oversee these activities and your company may be at risk of financial loss and/or criminal prosecution.

What is the role of the committee?

The role of the audit committee:

- Obtain an understanding of internal control and risk assessment

- Evaluate the effectiveness of the entity’s system of internal control

- Assess the qualifications, performance, and independence of the external auditor

- Review the terms of engagement (i.e., audit scope, risk assessment procedures)

- Identify matters that require attention by management

4 typical audit committee members

Membership typically includes:

1. Independent Director

2. Financial Expert

3. Public Officer

4. Non-executive Directors

Why do companies need independent auditors?

Not having a CPA firm as independent auditors is a conflict of interest. This can be a problem if the company fails to report information accurately or on time due to the fact that the independent auditing firm may have had some type of incentive to avoid reporting any issues with management’s decision-making process. An independent CPA assures shareholders that the company is properly prepared to create accurate financial reports.

Who is required to have an audit committee?

Typically companies with publicly traded stocks are required to have an audit committee. An example of how important it is can be found in the following mission statement, “We are committed to providing you with the financial information that allows you to determine your investment risk tolerance and enhance returns.”

Financial reporting has many functions, but one of its primary purposes is to provide information that enables investors and creditors to make more informed decisions.

What happens in an audit committee meeting?

The audit committee will usually meet once per month. At each meeting, an agenda is submitted in advance; however, some areas may arise that were not thought of in advance. If the board does not come to a decision on issues, they will usually schedule another meeting for further deliberation.

A usual meeting of an audit committee involves reviewing the financial statements of a company, audits by internal or external auditors, taxes, legal matters, and reports on credit issues. An outside auditor is assigned to attend the meeting to address questions posed by members of the board. The auditor ensures that all information given is accurate and complete, but also attempts to present any risks that may go along with the finances of your company. Members of the committee are usually able to ask questions and voice opinions during the meeting, but only members of the board are allowed to vote on decisions or motions.

How does the audit committee help in financial reporting?

Financial reporting has many functions, but one of its primary purposes is to provide information that enables investors and creditors to make more informed decisions. The use of financial statements in investing and lending decisions means there is a lot riding on how well you communicate the information on your company’s financial position, activities, and performance. To accomplish this task, all companies publish annual reports, but not every company has an audit committee to oversee their financial reporting.

What are the disadvantages of an audit committee?

The disadvantage of having an audit committee is that the members’ time is taken during work hours; therefore, their other duties may be put on hold. Another problem is when committees must reevaluate their own actions when they conflict with management’s suggestions or when the committee fails to meet all required deadlines during audits.

What are audit committee roles?

The role of an audit committee is to provide independent oversight, which includes responsibility for the integrity of financial reports and risk assessment. Members have the responsibility of identifying issues that management needs to focus on in their decisions. A typical role of the Audit Committee is to meet with executives on a regular basis to discuss any concerns about malpractice, risks, and the accuracy of any information that has been reported. The committee also recommends changes to accounting and financial reporting policies and practices and requires management to report on activities performed by internal auditors and external auditors.

In conclusion the internal audit function

To summarize this article, an audit committee is a group of individuals who are responsible for evaluating the effectiveness of policies and procedures designed to ensure accurate financial reporting. These members serve to provide independent oversight, which includes responsibility for the integrity of financial reports and risk assessment. The role of the audit committee is to supervise the auditing function, which includes financial statement preparation, management control systems, and risk assessment processes. This group of individuals is responsible for evaluating the effectiveness of policies and procedures designed to ensure that management’s representation of your company’s financial condition is true and accurate.

Caveats, disclaimers & audit committees

At ESG | The Report, we believe that we can help make the world a more sustainable place through the power of education. We have covered many topics in this article and want to be clear that any reference to, or mention of regarding financial statements, committee members, and the financial reporting process vs. the external auditors, internal audit for the board of directors, internal auditors vs independent auditors, audit committee’s charter, or internal controls in the context of this article is purely for informational purposes and not to be misconstrued as investment or any other legal advice or an endorsement of any particular company or service. We highly recommend that investors use a financial advisor, certified financial planner, or investment professional before entering the markets. Thank you for reading, and we hope that you found this article useful in your quest to understand ESG and sustainable business practices. We look forward to building a sustainable world with you.

Dean Emerick is a curator on sustainability issues with ESG The Report, an online resource for SMEs and Investment professionals focusing on ESG principles. Their primary goal is to help middle-market companies automate Impact Reporting with ESG Software. Leveraging the power of AI, machine learning, and AWS to transition to a sustainable business model. Serving clients in the United States, Canada, UK, Europe, and the global community. If you want to get started, don’t forget to Get the Checklist! ✅